Brazilian LTN Bonds

Here, for both your edification and reading enjoyment, is a story of yet another scheme of “bogus bonds” flying around the world of fringe finance.

The Brazilian Letra do Tesouro Nacional (LTN) bonds do have a root in history.

The real LTN bonds issued in the 1970’s were short, stop-gap measures, issued much like currency, but were issued to function as a “year-or-less IOU.” Inflation was rampant and it was easy to issue an IOU that could be paid with steeply inflated cruzeiros at a later date.

Cruzeiros were the currency of Brazil from 1942 to 1986 and again between 1990 and 1993(two distinct currencies). In 1986 a new currency which was introduced was called the Cruzado. After a few years, a new currency, the Cruzado Novo, or New Cruzado was introduced, only to be replaced in 1990 by the reintroduction of the Cruzeiro. In another attempt to control inflation in 1993, the government devalued the currency by taking off three zeros from the Cruzeiro and naming the new currency the Cruzeiro Real. The Cruzeiro was devalued several more times, and through the many devaluations, we at Aegis Journal calculate the actual face value of the bond in the current currency of realm, Brazilian Reals, to be .000000436 R. In US or EU – it is even less of a fraction of a cent.

Check out our calculations and the History of Brazilian Currency Devaluations

None of the LTN issues were for more than 365 days. Any cruzeiros that show a maturity dates of more than one year are an absolute FAKE – real dumb FAKE.

But wait, it gets worse…

Until the second half of the 20th Century, the Brazilian Government had issued public bonds in assorted occasions, to raise money to facilitate the nation’s development by specifically targeting infrastructure projects such as re-equipping ports and railways, increasing warehouse capacity, building cold storage rooms, building electrical power plants, and developing basic industries as well as development of rural areas. Like many countries both in Latin America and elsewhere, the government had borrowed more than they could pay back.

In 1957, the government of Brazil exchanged all of its debt which was issued from 1902 to 1955 for new bonds. Old debt holders had a five year window in which to make the exchange of old debt for new debt or face losing the value of their bonds. Thus, any Brazilian Bonds that were issued before 1955 are now worthless.

During the 1979-82 period, the Brazilian economy faced several adverse shocks:

(i) The 1979 oil shock;

(ii) Declining terms of trade, due to falling export prices and increases in the prices of imported capital goods and raw materials;

(iii) A global recession;

(iv) Unexpected increase in the international interest rates; and last but not certainly not least

(v) Breakdown of the international financing market for the indebted developing countries in September of 1982 (a typical case of market failure).

The growth strategy adopted by the Brazilian government after the first oil shock directly or indirectly promoted over-borrowing. The Brazilian default on external debt in the 80’s was the outcome of over-lending by creditor countries’ commercial banks – made possible in part by great international liquidity.

There was no institutional framework to deal with such problems. The main creditor countries organized under the IMF coordinated a strategy , which became known as “muddling through” This strategy did not work out because it did not address the fundamentals of the debt problem. This concerted action of creditor and debtor countries’ governments with the coordination of international organizations is a good example of government failure.

Only more than ten years after the beginning of the debt crisis, the Brady Plan,

proposed by the United States government, created a proper framework of cooperation and understanding between debtor and creditor countries to share the costs of wrong decisions taken in the past by reducing the debt service and the debt itself. In the second quarter of 1994, an agreement was signed between the Brazilian government and the international banks, by which the debt was securitized and transformed into several different bonds. (Source IMF)

So Brazil has restructured and/or exchanged old debt for new debt in 1964, 1983, 1984, 1986, 1987, 1988, and 1992 with the final Paris Club restructuring, and with commercial holders in 1988, 1991 and 1994.

No debt of the Brazilian government from 1970’s is any good by virtue of the Paris Club Agreements, IMF Agreements and as a result of the Brady Bonds / debt restructuring. Even if the debt holder’s orginal instrument was genuine and not a fake the bondsholders are nine internationally acknowledged debt-restructuring agreements behind.

Let’s also add to the festering pile of misinformation and outrageous lies the fact that you can buy these bonds in bulk from suppliers on Alibaba.com. Here are some page images of people selling Brazilian LTN Bonds, in bulk, on Alibaba see examples, 1, 2, 3.

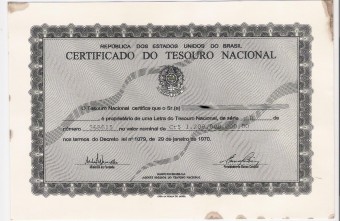

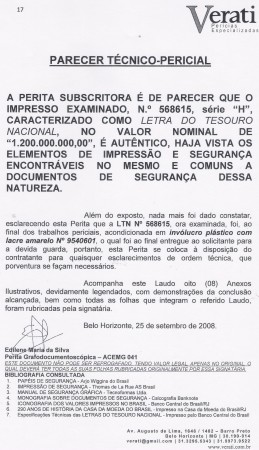

All bogus bonds inevitably come with a plethora of additional bogus documents to shore up the reality of the bogus note(s). They come with a Certificate to tell you the bond is real. How lovely! They may also come with an age appropriate Receipt.

My favorite is the Tax Statement showing the tax paid on the bond. The only problem with this pastiche is the idiots cannot figure out the difference between the old Cruzeiro and the new Real. It is almost as dumb as forging coins with a date like 22 B.C.

And let us not forget the required Verification that the bond or note is real issued by some independent third party who cannot be located.

Oh, as a final comment from the Central Bank of Brazil (BCB) the people who are debtors and who are supposed to pay the note owners. . .

The Central Bank of Brazil (BCB) has been receiving questions about bonds it supposedly issued under the names “Certidão Conjunta de Valor Atualizado”, “Certificado de Repactuação” and “Declaração de Autenticidade”. Such bonds, which carry the logo of the BCB, have allegedly been signed by some members of the Board and by other Brazilian officials.

The BCB herein informs that it is not allowed to issue any kind of Bond or debt note, pursuant to Complementary Act of Congress 101, of 4th of May, 2000.

Furthermore, all bonds and notes issued by National Treasury and held in custody in the Special System for Settlement and Custody (Selic), managed by the BCB, are book-entry, electronically registered and negotiated bonds and notes.

Hence, documents with the characteristics stated above are fraudulent and do not represent debts issued by the Central Bank or by the Brazilian government. The Federal Police have been duly notified about such occurrences.

Stop trading in these worthless fraudulent bonds and share this post with anyone you identify who is screwing with them.

{kind=link}

{kind=link}